VDP or Taxpayer Relief? Which one is right for you?

Finance Relief

Taxes

Ali Ladha, CPA, CA / May 8, 2026

When you’re in trouble with the Canada Revenue Agency (CRA), choosing the wrong relief program can be a costly mistake. The CRA offers a few major relief programs, but they are designed for very different scenarios.

As of the major policy overhaul in October 2025, the rules for coming forward to CRA have changed. Here is the definitive breakdown of Taxpayer Relief vs. VDP, and how to choose the right path for your situation.

Voluntary Disclosures Program (VDP): “Coming Clean”

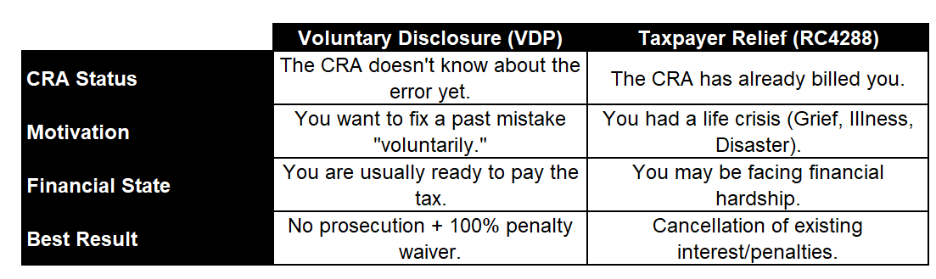

The VDP is for taxpayers who want to correct past errors before the CRA identifies them. This is the “Gold Standard” of relief because it provides protection from criminal prosecution and significant penalty waivers.

The “Prompted” Game-Changer

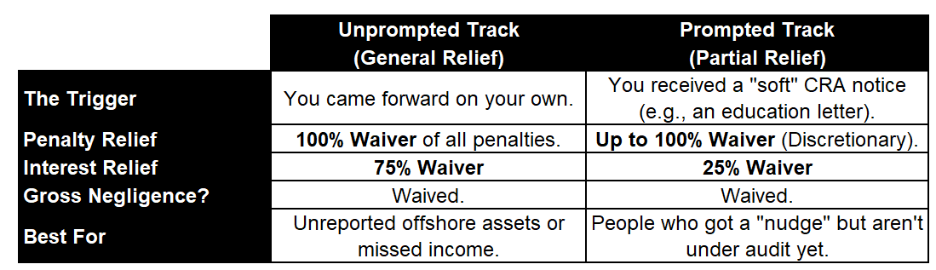

Previously, if the CRA sent you any letter, you were often disqualified from VDP. Now, some communication (like reminders to file or general education letters) allow you into the Prompted Track, giving you a second chance at relief that didn’t exist two years ago.

The Two Tracks: Prompted vs. Unprompted

Under the 2026 rules, the CRA has replaced the old “General vs. Limited” programs with two new tracks based on how you were “motivated” to come forward.

Taxpayer Relief (RC4288): The “Mercy” Path

Taxpayer Relief is used when the CRA debt, penalty, or interest has already been assessed on your account. Unlike the VDP, this is a request for mercy based on circumstances beyond your control.

- The Goal: To cancel penalties and interest because life made compliance impossible.

- The Criteria: Death in the family, serious illness, natural disasters, or CRA errors.

- The Limitation: It does not protect you from prosecution, and it doesn’t reduce the “Principal Tax” you owe, only the extra charges.

If you’d like to learn about the CRA Taxpayer relief program, read our blog post here.

Taxpayer Relief vs. VDP: A Quick Comparison

Payment Arrangements

If you have a tax balance you cannot pay in full, the CRA will not simply “wait.” Left unaddressed, the CRA has some of the most aggressive collection powers in Canada, including the ability to garnish your wages, freeze your bank accounts, and place liens on your home without a court order.

A Payment Arrangement is your primary shield. It is a formal agreement where you commit to paying your debt over a specific period. If the CRA accepts your plan, they will generally suspend these “legal warning” actions.

The Financial Disclosure Threshold (Form RC376)

The CRA doesn’t just take your word that you can’t pay your tax debts. Depending on the size of your debt and the length of your proposed plan, they will require a “Full Financial Disclosure.”

Individuals: You will likely need to complete Form RC376 (Statement of Income and Expenses and Assets and Liabilities). You must prove your monthly household income versus your “necessary” living expenses (housing, utilities, food, medical).

Businesses: You will need to provide up-to-date financial statements (Balance Sheet and P&L) and prove that the business remains a “viable” entity.

The Standard: The CRA expects you to try and borrow the money first (refinancing a home, line of credit, etc.). If you haven’t exhausted your credit options, they may reject your payment plan.

The Hybrid Relief Strategy: VDP + Taxpayer Relief

In many complex tax situations, a taxpayer may have multiple years of non-compliance, but their eligibility for relief varies from year to year. The Hybrid Strategy involves filing under two different legislative provisions at once to achieve the maximum possible debt reduction.

Phase 1: The “Prompted” VDP (Proactive Penalty Protection)

When the CRA sends an “Education Letter” or a general nudge about a specific income source (like unreported rental income), the taxpayer is often disqualified from the Unprompted (General) VDP track. However, they usually remain eligible for the Prompted Track.

How it works: You disclose the unreported income for all relevant years through the Voluntary Disclosures Program.

The Benefit: By using the Prompted Track, you can still secure a 100% waiver of gross negligence penalties and a partial waiver of interest (typically 25%).

The Goal: To “freeze” the situation and stop the CRA from starting a formal audit, which would result in 0% relief and massive penalties.

Phase 2: The Taxpayer Relief Request (Targeted Interest Cancellation)

While the VDP is excellent for removing penalties, its interest relief is often limited (especially in the Prompted track). To bridge the gap, a Taxpayer Relief Request is filed concurrently for specific years within that period.

How it works: For years where a specific “extraordinary circumstance” occurred (such as a medical emergency, a death in the family, or severe trauma), you submit a separate request for Interest Relief.

The Argument: You argue that while the VDP covered the “voluntary” disclosure of income, the taxpayer deserves a full 100% interest waiver for specific years because their life circumstances made it physically or mentally impossible to comply at that time.

The Goal: To recover the remaining 75% of interest that the VDP did not cover.

When to Use the Hybrid Strategy

This strategy is most effective for taxpayers who:

- Have multiple years of unfiled returns or unreported income.

- Have received some form of “soft” contact from the CRA (Education Letters).

- Can point to a specific “extraordinary event” that occurred during a portion of the non-compliant years.

Get Help Today

Understanding when to use the VDP program and/or the Taxpayer relief program is highly discretionary, and the quality of your written submission makes all the difference. At Tax Help Canada, we specialize in crafting persuasive, evidence-backed VDP and taxpayer relief requests to help you get back on track with the CRA.

Get in touch with us here.

The accounting and tax information provided in this post does not constitute advice and is meant to be for general information purposes only. The information is current as at the date of this post and does not reflect any changes in accounting and/or tax legislation thereafter. Moreover, the information has been prepared without considering your company or personal financial/tax circumstances and/or objectives.